Track the rise of instant payments.

FDIC-Insured - Backed by the full faith and credit of the U.S. Government

Major new study finds surging business interest in instant payments.

The adoption of instant payments is set to soar among U.S. businesses over the next two years, according to a new study by U.S. Bank.

What leaders need to know about instant payment adoption

The emergence of instant payments is transforming the landscape for how businesses move money – and by providing them with immediate access to funds, it has major implications for companies and how they manage their finances. While use of instant payments has been limited until now, a new study by U.S. Bank suggests it may have reached a tipping point.

Based on a large-scale survey of 1,420 finance leaders at businesses with revenue of over $100 million, the new U.S. Bank report reveals that 42% are using real-time payments through the RTP® network – up from 38% in our 2022 study. But more than two-thirds (68%) of companies say they expect to use instant payments via RTP or the Federal Reserve’s newly-launched FedNow® Service over the next two years.

So, what is driving the expected growth of instant payments? How are instant payments meeting front-office and back-office needs – and how can finance leaders prepare their organizations for a smooth addition of instant payments to their payment processes?

More Resources

Stay Connected

What are instant payments?

Instant or real-time payments enable companies to send, receive and request payments with immediate, irrevocable settlement of funds, 24/7/365 – evenings, weekends and holidays included.

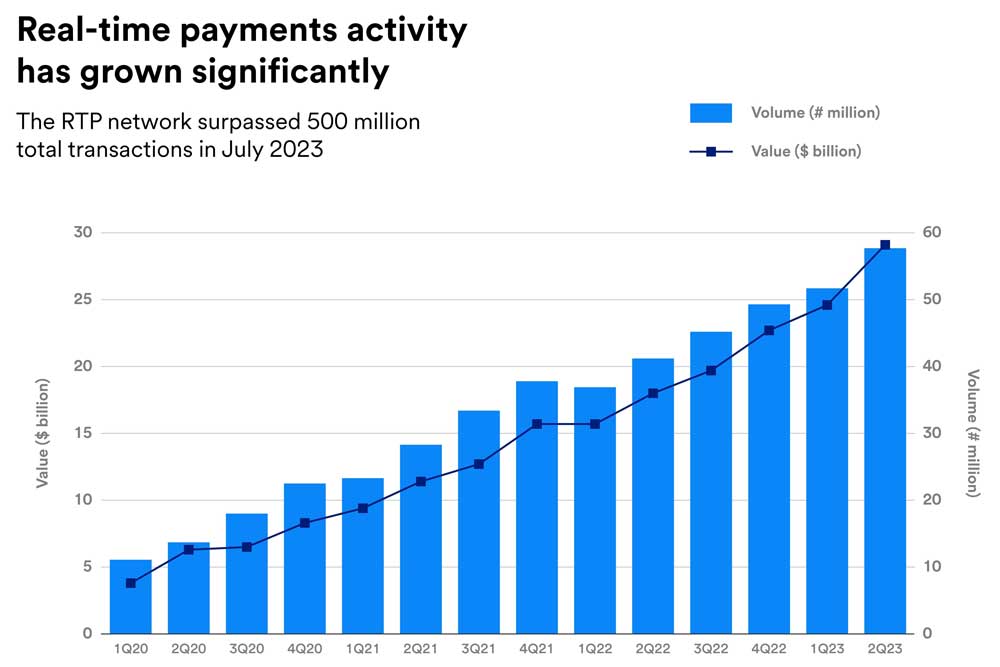

Instant payments may be made through the RTP network, operated by The Clearing House, which provides payment settlement to enrolled U.S. financial institutions currently covering 65% of U.S. demand deposit accounts. The FedNow Service, launched in July 2023, is a new instant payment infrastructure developed by the Federal Reserve that will enable financial institutions of every size across the U.S. to provide safe and efficient instant payment services. Many banks that participate in the RTP network will also use the FedNow Service to deliver the full reach of instant payment endpoints.

65% of U.S. demand deposit accounts are covered by the RTP network.

The rapid rise of instant payments

Instant payments usage has increased steadily in recent years, and businesses expect to use them even more. More than 7 out of 10 companies in sectors like consumer and retail, hospitality and leisure, and healthcare expect to use instant payments within two years, as consumers continue to demand faster payment options. We surveyed finance leaders to get their views on the adoption of instant payments and compiled the data into an infographic.

Exploring the business case

Instant payments offer various advantages. Key among them, of course, is 24/7 immediate access: by eliminating the time between sending and receiving funds, businesses can have more control over their money. This isn’t just a theoretical advantage. In our survey, 46% of finance leaders say that immediate availability gives their company better working capital – making it the top reason for business’s interest in instant payments.

It’s not all about speed, though. Errors are reduced and processes simplified, including reconciliation. Each payment can include transaction data, such as remittance information to enable straight-through payment processing, resulting in improved analysis and planning, and vastly simplified financial management.

The benefits expand beyond the back-office. In fact, adoption of real-time payments to date has largely been driven by customer payment or ‘front-office’ requirements, as businesses adapt to evolving consumer expectations. Now, 43% of the businesses surveyed say improving the customer and/or vendor payment experience is driving their interest in instant payments.

“Consumers are used to using services like Venmo® and Zelle® and expect immediate transactions with companies, whatever time or day it is,” says Mike Jorgensen, head of Emerging Solutions and Strategy at U.S. Bank. These demands carry over to when funds are required from a company, too – such as an emergency insurance disbursement. Instant payments are critical here.

Back-office tasks, by comparison, have seen less adoption – but appetite is growing. For instance, because instant payments are available 24/7 every day including weekends and holidays, they are ideal for paying vendors on a specific due date, emergency payroll or vendor payments, immediate payment of non-payroll expenses including travel and relocation, and meeting emerging needs such as payroll-on-demand systems for serving the growing freelance workforce.

46% of finance leaders say that immediate availability gives their company better working capital.

“Consumers are used to using services like Venmo® and Zelle® and expect immediate transactions with companies, whatever time or day it is.”

Mike Jorgensen,

Head of Emerging Solutions and Strategy, U.S. Bank

Factors underlying future adoption

Growth of instant payments in the next two years will be driven by multiple factors. As the FedNow Service is adopted by smaller banks and credit unions, instant payments will become available to many more demand deposit accounts. Increased ubiquity will help tilt the scales for many businesses in favor of adopting instant payments for the first time, or using them in more situations. Demand will also grow as more businesses become digitally enabled across their finance operations, making it easier to start using instant payments. As a result, instant payments are likely to start being used where many businesses currently use wires, which are relatively expensive, do not offer full 24/7 service and are not immediate.

But some things will need to change for instant payments to become truly ubiquitous. “Businesses need to know that instant payments will work smoothly for all their needs, without issues, to be comfortable about switching to instant payments at scale,” says Mike Jorgensen.

One aspect that needs to change, he suggests, is the transaction limit: RTP has a transaction cap of $1 million while the FedNow Service limit is $500,000. These caps prevent instant payments from being used in larger and more complex transactions, ruling them out for many back-office functions. Instant payments also needs to extend its reach, which can only happen if more banks offer this type of payment. Finally, certain barriers need to be overcome to ease adoption, including enabling request for payment, interoperability between real-time payment networks, and integration with value adding services such as directories and remittance information.

Switching to instant payments: steps for a smooth transition

Whether they are dipping their toe into the world of instant payments for the first time or rolling them out for new use cases, there are five key areas where financial leaders should focus to prepare their business – and maximize the benefits.

1. Define the destination and map the journey ahead.

Moving to instant payments is a journey – one that is different for every business. Defining clear business objectives and aligning around them is essential so everyone involved understands the direction. So too is mapping the steps the business needs to take: every organization has a different starting point and varied requirements. “Digitally native businesses and those already employing cloud platforms have a head start on those that remain heavily paper-based and check-based, because they already have some of the technology infrastructure in place”, says Anu Somani, head of U.S. Bank Global Payables and Embedded Payments. Evaluate your current position to determine the best path forward.

2. Assemble a multidisciplinary team.

Instant payments affect multiple parts of an organization, so the finance team shouldn’t be solely responsible for implementation. For instance, digital and technology teams will manage APIs and interoperability with other systems and ensure data security. Legal and human resources teams can also play a part. For many businesses, customer experience and product leaders are key, as they drive the use of instant payments as a core part of business strategy and their efforts to improve customer experiences.

3. Build your digital capabilities.

Instant payments’ full benefits can only be delivered if a company is digitally advanced. That includes shifting away from electronic data interchange-based systems towards API-driven ones. It also means building robust data management systems. For checks, organizations only need the most basic information about payees – but digital payments require much more data about customers, vendors and employees. Security should be front of mind, with robust technology and processes to avoid data breaches.

4. Be ready to manage money 24/7, every day of the year.

Finance leaders and their teams need to scrutinize every detail and all the implications of switching to instant payments – because money will be moving outside of traditional banking hours. When they enable after-hours and weekend payments, companies may realize that nobody is available to ensure that accounts are funded, for instance. A trusted partner can provide guidance on building always-available treasury management solutions.

5. Pick a partner.

“A lot of our clients want to extricate themselves from the complexity of managing instant payments by partnering with a fintech or bank,” says Anu Somani. They may also work with select technology platforms to handle implementation and manage ongoing stakeholder payment preferences. Picking the right partner can significantly reduce the work involved in adopting instant payments, thereby ensuring that the business can stay focused on its goals.

Many businesses are already taking advantage of instant payments, and their numbers are set to rise sharply in the coming years. Instant payments are a vital tool for today’s digitally enabled businesses – and, in the future, could end up transforming money movement.

Read the newest data on instant payments.

We’ve put together a helpful infographic to illustrate trends in instant payments, including how often they are being used, what types of companies are using them most and what finance leaders are saying about further adoption of RTP and the FedNow Service in the future.

More insights from our research.

Economic insights

Is the economy doing better than you think?

California Report

California finance leaders respond

HEALTHCARE INSIGHTS

Top priorities for healthcare finance leaders

DIGITAL TRANSFORMATION

Leaders investing in digital technology

Read the full 2023 CFO Insights Report.

Discover how the finance function is repositioning itself as a driver of change by focusing on cost control, digital transformation, talent acquisition and retention, instant payments and more.

Start of disclosure content