Turn risk into opportunity with supply chain finance

Webinar: What’s new in international payments?

Best practices on securing cardholder data

Webinar: Managing foreign exchange risk in unpredictable markets

Hospitals face cybersecurity risks in surprising new ways

Webinar: Robotic process automation

Tactical Treasury: Fraud prevention is a never-ending task

Post-pandemic fraud prevention lessons for local governments

Webinar: Empower your AP automation with strategic intelligence

Webinar: Building digital bridges for treasury optimization

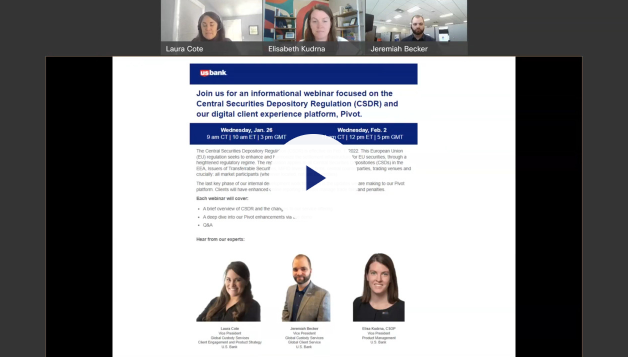

Webinar: Recording of the Central Securities Depository Regulation and Pivot

Evaluating interest rate risk creating risk management strategy

Authenticating cardholder data reduce e-commerce fraud

Webinar: Digitize your AP processes to optimize results

Risk management strategies for foreign exchange hedging

Webinar: AP automation—solve payment challenges with an invoice-to-pay solution

What is CSDR, and how will you be affected?

Webinar: CRE technology trends

Webinar: The future of digital onboarding for U.S. Bank clients

Webinar: Driving innovation to impact treasury management

Webinar: CRE treasury leader roundtable

Proactive ways to fight vendor fraud

Webinar: Redefine your business with technology

Webinar: Economic, political and policy insights

4 tips for protecting your business against Coronavirus-related scams

The latest on cybersecurity: Mobile fraud and privacy concerns

Webinar: The impact of innovation on processing receivables

5 Ways to protect your government agency from payment fraud

Redefining beneficial ownership in the Cayman Islands

Cayman Islands’ Private Funds Law: What you need to know

The latest on cybersecurity: Vulnerability testing and third-party software

Webinar: International payments

5 steps you should take after a major data breach

Fight the battle against payments fraud

Cybercrisis management: Are you ready to respond?

Complying with changes in fund regulations

The cyber insurance question: Additional protection beyond prevention

Protecting your business from fraud

The password: Enhancing security and usability

Avoiding the pitfalls of warehouse lending

Fraud prevention checklist

Why KYC — for organizations

Cybersecurity – Protecting client data through industry best practices

Business risk management for owners of small companies

Government agency credit card programs and PCI compliance

BEC: Recognize a scam

How to improve your business network security

Increase working capital with Commercial Card Optimization